Hello everyone, do you know what is FIRE? 🔥

Imagine a life where you no longer have to work, where your time is entirely your own, and financial stress is something you no longer have to about. This isn't a distant dream but a reality for the people who have embraced the FIRE movement. FIRE, which stands for Financial Independence, Retire Early, is a lifestyle and financial philosophy that's gaining traction worldwide. Let’s explore what FIRE is, how it works, and whether it might be the right path for you.

The idea behind this movement is to start saving as much as possible, reducing the unnecessary expenses and invest a large portion of your income. The investments should be diversified and their compound interests helps you to grow your wealth. The accumulated wealth should be enough to live off the passive income generated by your previous investments

If you estimate to spend lower than 18.000 € per year (i.e., 1.500 € per month) and you want to be covered for 30 years, you need to save at least 540.000 € (even more considering inflation), but if you follow a FIRE approach, the investments can help you to reach the same independence with a lower amount of money.

Please it is important to conduct your own research and consult with a professional financial advisor before making any investment decisions. The content presented below should not be construed as financial advice, recommendations, or endorsements of any specific investments or strategies. Your financial situation is unique, and you should tailor your decisions to your personal circumstances and goals.

The 4% Rule

The 4% Rule of the FIRE movement is the most popular way to find exactly how much money you need to save to achieve financial independence and retire early. The 4% rule suggests that you can withdraw 4% of your retirement savings annually and your savings should last for at least 30 years without running out. This rule of thumb helps retirees estimate a safe withdrawal rate from their investment portfolios to sustain their standard of living.

Below there is the step-by-step explanation with some numbers:

- Determine Annual Expenses: estimate your annual expenses in retirement. For a medium Italian person, we can estimate about 18.000 € (i.e., 1.500 € per month).

- Calculate Your FIRE Number: this is calculated by multiplying your annual expenses by 25 (this number comes from the 4% withdrawal rate). For a medium Italian person, the FIRE number is 450.000 € (i.e., 18.000 € × 25).

- Calculate Annual Withdrawals: according to the 4% rule, you can withdraw 4% of your total savings the first year to cover your annual expenses, then multiply the previous withdrawal for the inflation rate (e.g., 2 %). For a medium Italian person, the first annual withdrawal is about 18.000 € (i.e., 450.000 € x 0,04), the second annual withdrawal is about 18.540 € (i.e., (450.000 € x 0,04) x 1,3), etc.

Is the 4% rule accurate? Obviously not because it makes the following assumptions:

- Your expenses will be the same every year, except for inflation.

- Your investment portfolio consists of 50% stocks and 50% bonds.

- The retirement time is fixed to 30 years.

- Future market conditions will be similar the previous ones.

- There are no taxes on capital gains.

How to achieve FIRE in Italy?

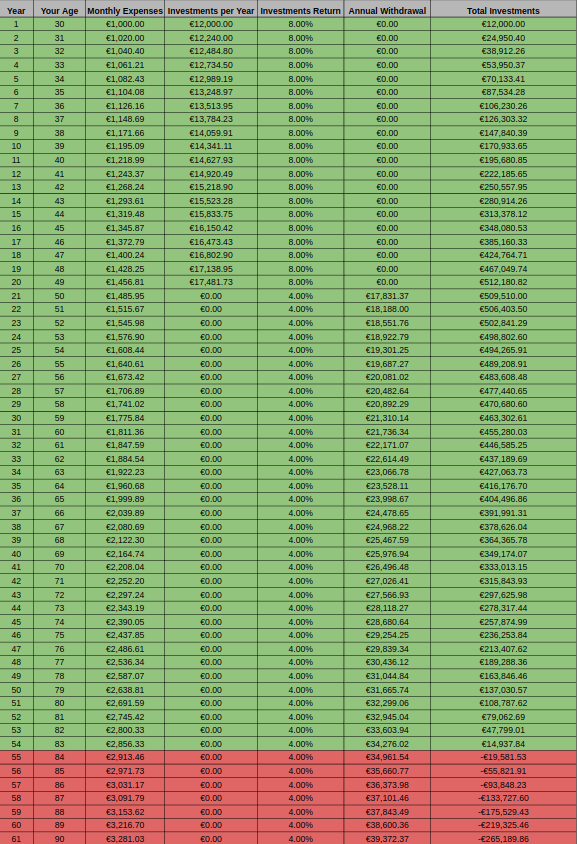

It is not simple to estimate the right amount of money to invest in Italy to retire at 50 years old because it highly depends on your lifestyle and your monthly expenses. However, I tried to create a Google Sheets table to represent an Italian person with an initial net salary of 2.000 € and the following conditions:

- He/She starts investing at 30 years old

- His/Her initial monthly expenses are 1.000 €

- The annual inflation rate is 2 %

- An investment return per year of 8 % before retirement and 4 % after retirement

- He/She invests 1.000 € per month

- He/She increases by 2 % his/her investments each year

- He/She retires at 50 years old

- Taxes on capital gains at 26 %

As you can see from the following table, he/she would be able to retire at the age of 50 and cover all his/her monthly expenses for more than 30 years (maybe more if you also consider the Italian pension).

If you want to play with the parameters (age, monthly expenses, etc.) you can download the following sheet and change the default values on the right:

Please share your opinion below and let’s build a supportive and informative community together! 🤝